The regular Monday recap is out! Read it to keep up with what happened last week.

On Thursday, we turned our attention to the monetary policy meeting of the European Central Bank (ECB), which kept its key interest rate at 4.5 %. This is a record high level.

On Thursday we also got some data from the US, which was rather negative for the USD. According to the preliminary estimate, the US economy (GDP) grew by 3.3 % in Q4.

On Tuesday night we got the New Zealand inflation data which resulted in the NZD strengthening. The core annual inflation rate fell from 5.6 % to 4.7 %.

The Bank of Japan met on Tuesday morning and left the rate unchanged at -0.10 %. In any case, the BoJ kept the door open for a possible policy change.

The market calmed down after the ECB meeting and the price lost momentum still around our previous zone of interest. This morning's data on Tokyo inflation confirmed our continued outlook.

We start the week with Tuesday's data from the Japanese labour market, namely the unemployment rate, which is expected to remain unchanged (00:30). In the morning, we will also have preliminary data from Australian retail sales, which are estimated to fall (01:30). In the morning, we will focus on preliminary GDP in the euro area (11:00).

Monday's recap is here! We have a couple of central bank meetings this week. Let's hope something comes of it. Have a great Monday, everyone!

We started the week with a speech by Robert Holzmann (ECB), from which we could understand that monetary policymakers should probably not discuss any early rate cuts just yet.

On Tuesday, we got fairly strong data from the UK labour market, on which the pound strengthened. The unemployment rate remained steady at an estimated 4, 2 %.

The US Dollar received fairly positive data last week, which reinforces our belief that the USD has been stronger and increasingly interesting since the new year.

On Tuesday, we also received data from Canada. The annual core inflation rate fell to 2.6 %, but the core annual rate rose to 3.4 %, as expected.

The Australian has had a tough week. The inflation rate was 3.9 %, which was in line with market forecasts and was no change.

To make matters worse, we also focused on inflation from Japan, which came out lower and negative for the JPY.

The week starts with Tuesday's Bank of Japan meeting, which is not expected to bring any change in rates. However, it could offer some signal of its willingness to normalise rates in the spring. That could move the JPY quite a bit.

Monday's recap is here! Join us as we recap the highlights of what happened last week!

Last week, we focused mostly on Tuesday's unemployment rate from the eurozone, which was positive for the euro.

We got a bit more interesting data from the US. Thursday's inflation was positive for the USD as the core inflation rate rose to 3.4 %.

Tuesday's Tokyo inflation data was negative for the JPY. Tokyo's core CPI index declined to 2.4 % in December.

We are in for a week of inflation. On Tuesday, we turn our attention to the inflation rate in Canada, which is expected to rise slightly. On Wednesday morning, we will see inflation data from the UK, where we are again expected to see lower numbers.

Sources:

The first Monday recap of the new year is here! Join us as we recap what moved the markets over the past week. We wish you a successful start to trading in the New Year 2024!

On Friday, we focused on the preliminary inflation data from the euro area, which turned out to be mostly positive for the euro. The core inflation rate rose to 2.9 % year-on-year in December

The US dollar had a volatile week, helped by the labour market reports. Thursday's jobless claims fell to 202k.

Canada's unemployment rate remained unchanged in December, but at a 22-month high.

This week will be a bit more relaxed, but we will still have some interesting data.

Tuesday (00:30) sees the release of data on the Tokyo inflation rate, where a slight reduction is expected. Later in the morning (7:45), data from the Swiss labour market will be released, where a slight increase in the unemployment rate is expected.

Sources:

The week has gone by like water and we have a new Monday recap for you, packed with fundamentals from last week!

The European Central Bank (ECB) met on Thursday and is expected to leave its key interest rate unchanged. The interest rate is at multi-year highs.

We also got a similar scenario at the Bank of England (BoE) meeting, which left the base rate unchanged.

The most important fundamental that we focused our attention on was Wednesday's Fed meeting. The Fed left rates unchanged, as planned, at 5.5 %.

Apart from interest rates, on Thursday we also watched data from the Australian labour market, which turned out to be positive for AUD.

Last Thursday's meeting was held by the Swiss National Bank (SNB), which also left the key interest rate unchanged at 1.75 %.

This week will be mostly about inflation.

The week starts with the Bank of Japan meeting on Tuesday (4:00), where no change is expected. Let's see if we get any clues on the planned changes in the FX market.

Later at 11:00 we will turn our attention to the current inflation rate in the euro area and at 14:30 in Canada.

Sources:

The regular Monday recap is here! Together, let's recap the highlights of the past week.

On Wednesday, we watched incoming data on GDP and retail sales in the euro area. Retail sales fell by 1.2 % yoy in October. This is the third straight month of decline.

The news from the US labour market was the most important fundamental on which we focused our attention. Unemployment claims rose again to 220k. It was the second highest reading since September and negative for the USD.

From Japan, we saw some surprising news last week that added quite significant volatility to the JPY market. On Thursday, the BOJ Governor visited Prime Minister Kishida's office where he was due to confirm his outlook for wage increases next year.

This week will be quite nutritious.

On Tuesday, we have UK labour market data (8:00) followed by US inflation figures in the afternoon (14:30). This will certainly be the market's focus in conjunction with last week's labour market developments.

With the Fed's monetary policy meeting on Wednesday (20:00), Tuesday's inflation data will be all the more important.

Sources:

The regular Monday recap is out! Let's take a look together at what news moved the market last week, and what we'll focus on in the current one.

On Thursday, we were expecting quite important data on inflation in the euro area and the labour market. The core inflation rate fell to 2.4 % in November. This marked the lowest reading since July 2021 and was below estimates.

On Wednesday we got some GDP data that was positive for the USD. The US economy grew by 5.2 % in Q3.

The Canadian hasn't had a great week. Thursday's Q3 GDP fell by 0.3 %.

An important fundamental we watched was Wednesday's meeting of the Reserve Bank of New Zealand. The NZD strengthened in response to the meeting.

At the end of the week, we still got data from the Japanese labour market, which turned out positive. The unemployment rate unexpectedly fell to 2.5 %.

On Tuesday, we will wait for the incoming Tokyo inflation data (00:30). And later at 4:30 will come the RBA meeting where the base rate is expected to remain steady at 4.35 %.

Sources:

The regular Monday recap is here. Last week we were mainly interested in the Canadian inflation rate and the US labour market.

Have a nice Monday!

On Thursday, we watched the incoming Eurozone PMI data, which turned out to be positive for the EUR.

On Thursday, positive PMI data also came in from the UK, beating market expectations.

From the US, we were most interested in the labour market numbers. Specifically, unemployment claims, which we received on Wednesday, because Thursday and Friday were holidays in the US.

The most important news from last week was Tuesday's inflation in Canada, which was not very positive for the Canadian dollar.

The week will start with Tuesday's Australian retail sales figures (1:30), which according to preliminary estimates should fall slightly.

Wednesday will be more interesting as the Reserve Bank of New Zealand's monetary policy meeting is scheduled (2:00), where a pause is expected. Then we get the preliminary US GDP data in the afternoon (14:30).

Sources:

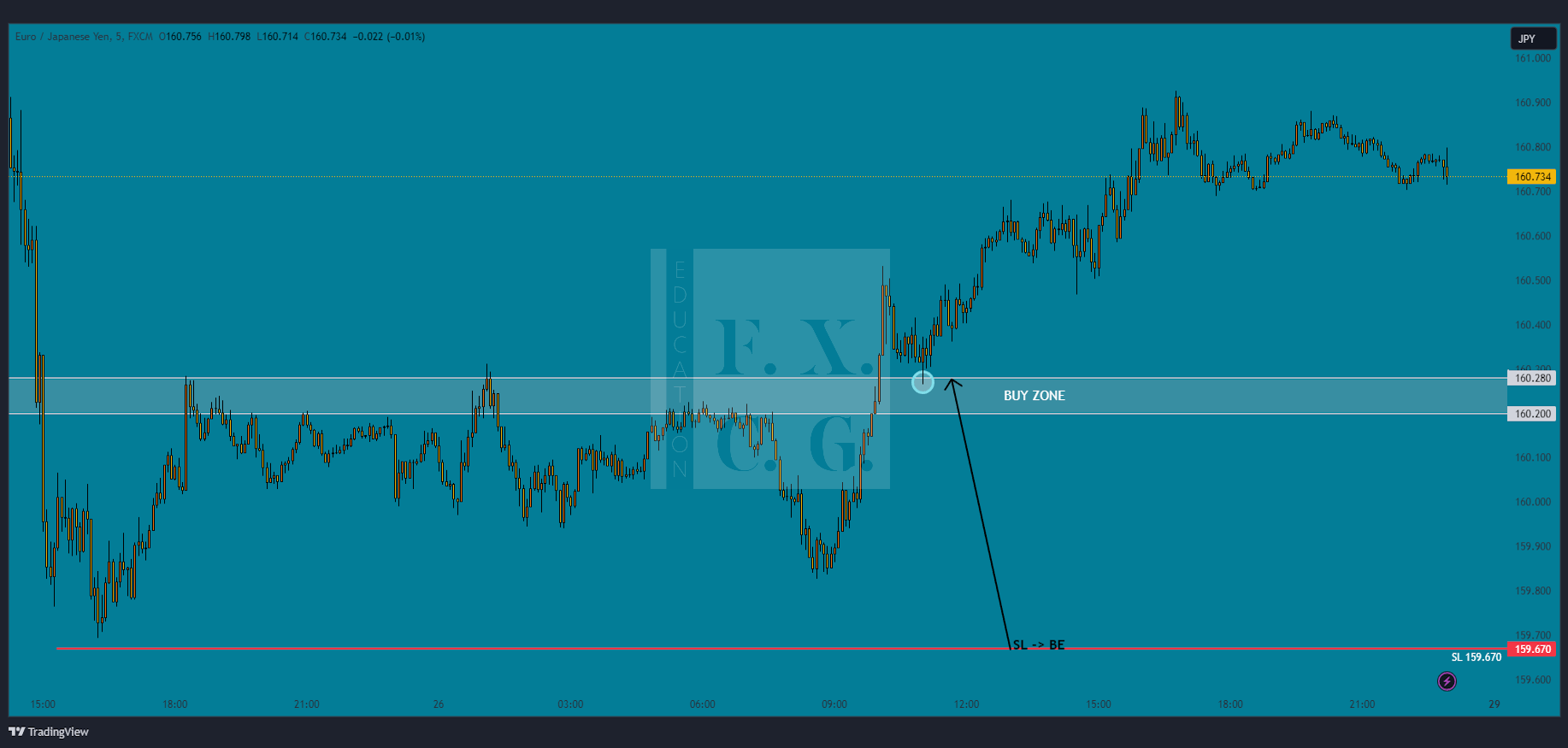

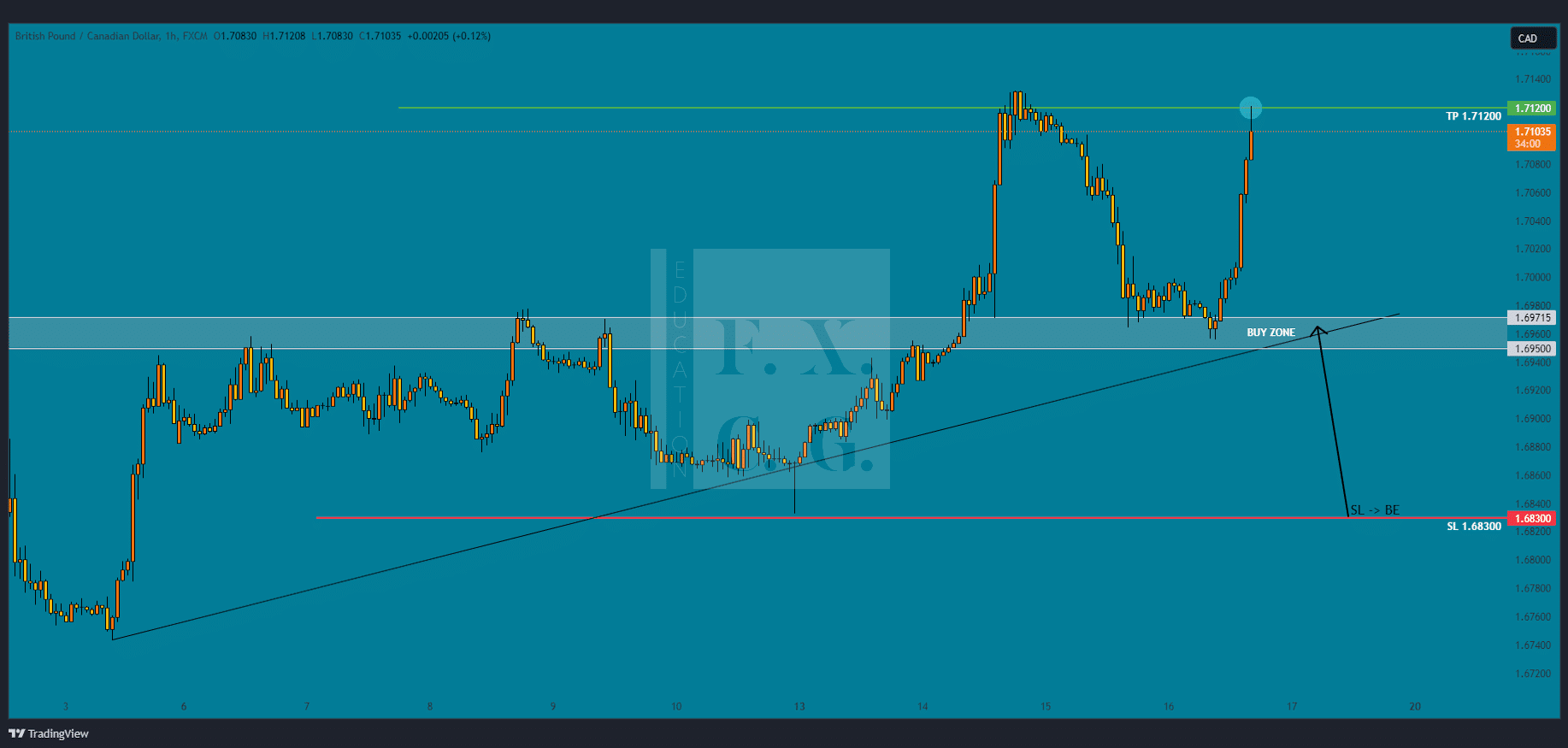

Last week, we focused mostly on inflation and labor market data, which provided a trading opportunity on BP/CAD.

Let's recall together what was central.

Tuesday's euro area labour market data were broadly positive. According to preliminary data, the number of employed persons increased by 0.3 % in the 3 months to September 2023.

On Tuesday we also got labour market data from the UK, which was positive for the pound.

The most important news the market focused on last week was the current inflation rate in the US.

The Canadian dollar also weakened in response to the US data. As a result, we decided to take advantage of the trading opportunity on the currency pair GBP/CADthat we shared in the discord group.

The more interesting data to focus on will come on Tuesday, when the latest Canadian inflation numbers are released (14:30).

Sources:

Monday's recap is here! Let's recap together the most important events that moved the markets last week.

From the euro area, we got retail sales and PMI data last week, which were rather negative for the euro.

Friday's data on the UK economy were quite positive.

Thursday's numbers from the US labour market were again generally good. The number of Americans applying for unemployment benefits decreased by 3 thousand.

Our attention was mainly focused on Tuesday's monetary policy meeting of the Reserve Bank of Australia (RBA), which, as expected, raised the interest rate by 25 basis points.

On Tuesday we got more data from the Swiss labour market, which looked good.

We received data from the Czech Republic last week to which the koruna reacted by strengthening. The unemployment rate fell from 3.6 % to 3.5 % in October.

This week will be mostly about inflation and the labour market.

On Tuesday, we get UK labour market data (8:00), followed by preliminary Eurozone labour market and GDP numbers. In the afternoon, the market will turn its attention to the latest inflation rate from the US.

Sources: