Monday's recap is here. Together, let's recap the highlights of the past week. And that was.

On Tuesday, we watched the preliminary PMI data from the euro area, which came out negative for the euro.

On Tuesday, we focused our attention on the UK labour market data, which was incomplete.

Tuesday's PMI, came out positive for the USD. The manufacturing index rose to 50 points, beating market estimates.

On Wednesday, we focused our attention on the Bank of Canada meeting. The Bank of Canada left the key interest rate unchanged as planned.

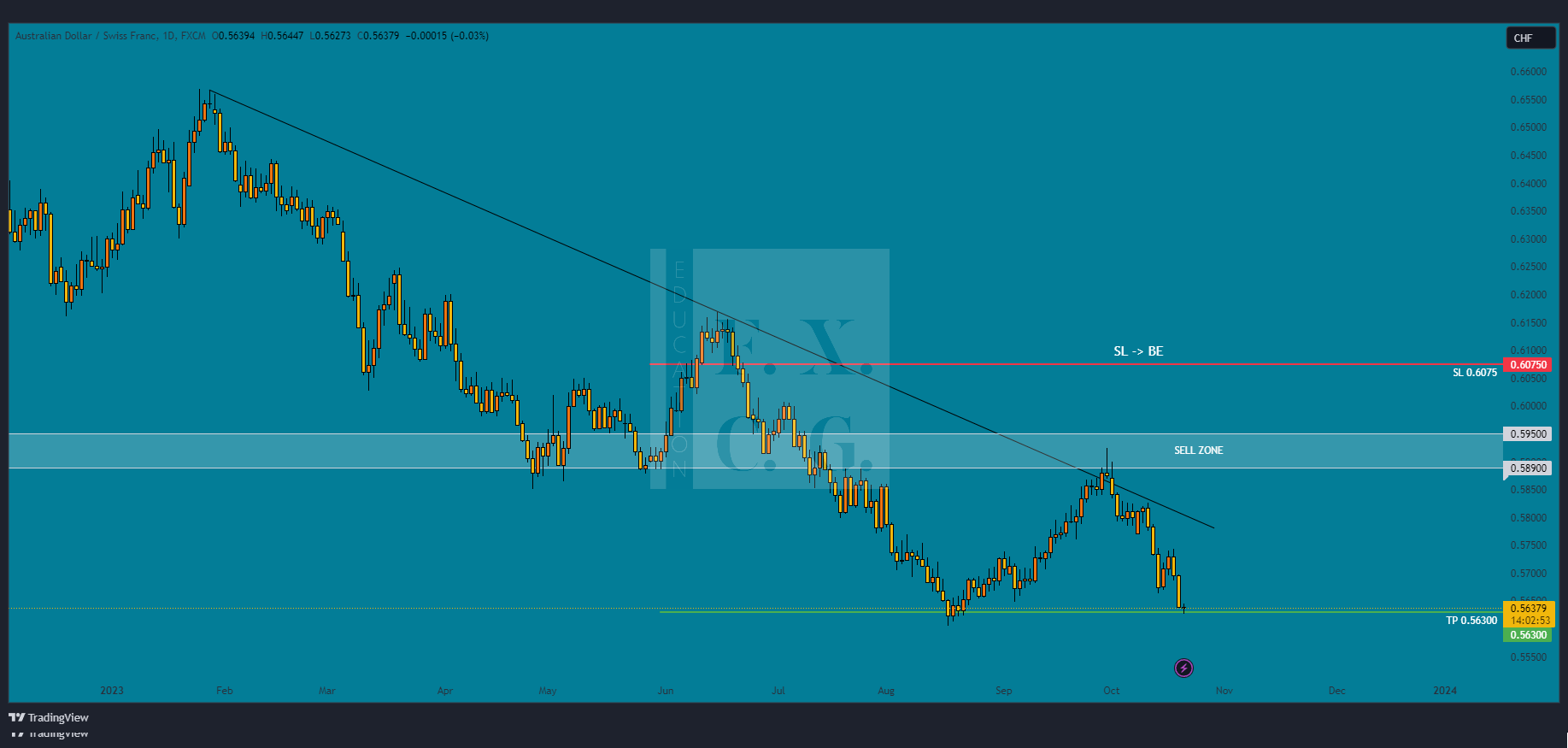

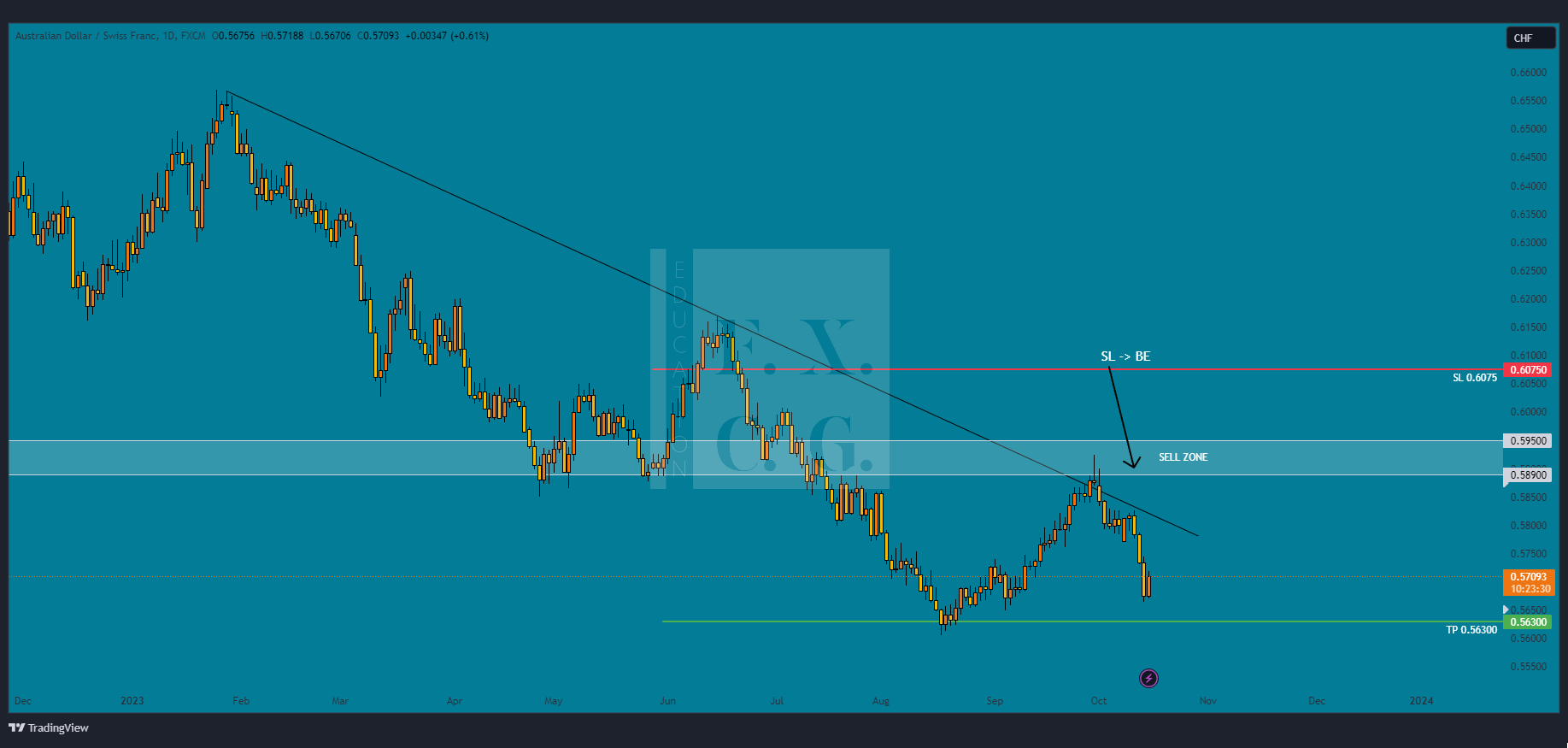

The Australian dollar had a fairly positive week, strengthening mostly on strengthening quarter-on-quarter inflation.

Tuesday will be mostly about Japan (JPY). Overnight, unemployment rate data will come in, accompanied by retail sales and the Bank of Japan meeting at 3:30. Again, the BoJ is not expected to raise rates, but we could already hear that a hike plan is on the table.

Sources:

Welcome to our regular Monday recap of the past week. It was full of inflation data. Let's recap the highlights together.

Wednesday's inflation rate in the euro area came in line with market expectations. The headline annual inflation rate declined to 4.3 % and the core rate fell to 4.5 %. Which is the lowest reading since August 2022.

On Wednesday, we also watched the UK inflation rate, which remained at 6.7 %, holding at an 18-month low, according to market estimates.

On Tuesday, we also got inflation data from Canada. The year-on-year inflation rate fell to 3.8 %, which was below market expectations.

Thursday's Australian labour market data supported our technical outlook on AUDCHF and helped TP.

This week will be interesting from a fundamental point of view, as several central bank meetings are scheduled.

On Tuesday, we'll focus on the Japanese inflation rate (2:30) and a flurry of preliminary PMI data from Australia, the Eurozone, the UK and the US. In the morning (8:00), UK labour market data will add to the mix.

Sources:

The regular Monday recap is here! Together, let's recap the highlights of the past week.

Last week was pretty weak on data... But that can't be said for the USD. US data played a significant role throughout the week. On Wednesday, the actual PPI numbers came out, which were surprisingly positive and good for the USD.

The next event we focused on was Friday's Swiss PPI numbers. Producer and import prices fell by 1.0 % yoy in September.

We have shared our 2 outlooks on the AUDCHF and NZDCHF currency pairs to the discord group. Currently we have all positions protected from possible loss.

The current week will again be richer in incoming data.

On Tuesday, we will focus on UK labour market data, which will come at 8:00. The unemployment rate is expected to remain steady (albeit quite high).

Sources:

A new trading month is upon us and how else to start it than with a review of the most important things that happened last week. Read on to keep up to date.

On Friday, we got the preliminary Eurozone inflation numbers, which came in lower.

Like every Thursday, we were interested in the numbers on initial claims for unemployment benefits in the US.

Tokyo core inflation fell from 2.8 % to 2.5 %, marking the third consecutive month of decline.

During the week, we posted our view on the USD/CZK currency pair to the outlook group, where we entered directly into the CNB meeting. Here, the aforementioned fundamentals that weakened the CZK played out beautifully.

This week will be a bit more interesting.

On Tuesday, we have the RBA meeting, where the central bank is expected to leave rates unchanged. At 8:30 we will then be treated to data on the current inflation rate in Switzerland.

Sources:

Welcome to our regular recap and outlook. Last week was literally a week of central banks and inflation. Let's recap the most important news together.

Earlier in the week, we focused our attention on inflation from the Eurozone, which came a few days after the ECB meeting. The annual rate fell in August to its lowest level since January 2022.

Last week was a very nutritious one for GBP and the negative data only reinforced our view that it is weakening. On Wednesday (the day before the BOE meeting), we were waiting for actual inflation rate data from the UK. The annual core inflation rate fell to 6.7 % in August from the previous 6.8 %.

On Wednesday, the Fed left the benchmark interest rate unchanged, as expected. However, the US dollar strengthened in response to the press conference.

This week will be much weaker. On Tuesday, we will focus on the current inflation rate in Japan. On Thursday, we will await initial jobless claims in the US.

Sources:

Here is our regular summary and outlook. This week will be very rich from a fundamental position and we expect bigger moves. So stay tuned so you don't miss anything!

The most important event of the week was Thursday's ECB meeting, which surprised with a 25bp increase in the base interest rate.

In the group we shared our trading outlook (long) on the EUR/AUD currency pair, which has entered the first zone of interest thanks to the ECB.

The British pound had a week full of bad data, to which it reacted by weakening.

Other interesting data we were waiting for were the US labour market and inflation numbers.

Thursday's data from the Australian labour market was negative for AUD and only supported our outlook on the EUR/AUD pair.

The current trading week will be very interesting from a fundamental position and we expect significant moves.

It will all revolve around inflation and central bank meetings. Here are the most important news stories we'll be focusing on this week:

Tuesday, September 19: Eurozone (11:00) and Canadian (14:30) inflation rates

Wednesday, September 20: UK inflation (8:00) and Fed monetary policy meeting (20:00)

Sources:

Welcome to our regular Monday recap. Together, let's recap what moved the markets last week, and what we'll have in our sights this week.

Thursday's GDP data from the euro area came out rather negatively for the euro. In fact, euro area GDP increased by 0.1 % in the three months to June 2023 compared to the previous quarter, which is lower than the initial estimate of 0.3 %. This is not good news.

As every Thursday, we were interested in the US news regarding new unemployment claims.

On Tuesday, we focused our attention on the Reserve Bank of Australia meeting. At its meeting, the Bank of England kept its rate at 4.1 %

On Tuesday, we will be interested in the latest data from the UK labour market, which will come at 8:00 am.

On Wednesday, the markets will focus on US inflation, which will come at 14:30. Here we will expect increased volatility as it could affect the Fed's next steps.

Sources:

We start the new month with a summary of what happened in the last week of last month. It was mostly about data from America, which added volatility to the market.

Let's remind ourselves together of the most important things.

On Thursday, we focused on data on the unemployment rate in the euro area. It remained unchanged in July at a record low of 6.4 %.

Thursday's data on new jobless claims in America surprised and fell by 4k vs. market expectations to 228k.

The beginning of the week will be quiet because it is a holiday in America and Canada.

On Monday, we will focus on Swiss GDP (9:00) and the afternoon outputs of the European Central Bank members.

We wish you every success in the new month. Have a great month!

Sources:

Welcome to our regular Monday recap of a fundamental worth remembering. Last week didn't bring much to the markets, but a few things caught our eye nonetheless.

Have a nice Monday everyone!

On Thursday, in a relatively quiet week, we focused on data from the US labour market.

Wednesday's Canadian retail sales data came in tentatively on par with the previous month.

We also got retail sales data from New Zealand on Wednesday, which showed better-than-expected numbers.

This week we will focus our attention mainly on the second half of the week.

On Thursday, we are due to see the preliminary inflation rate numbers from the Eurozone, which will come at 11:00 and will be accompanied by the unemployment rate, which is estimated to remain stable at 6.4 %.

Sources:

Hi, everybody! Here is the regular Monday recap of what we watched in the last trading week. You will also find our executed trade that we posted to our group.

Friday's euro area inflation data came in as expected. The annual core inflation rate fell to 5.3 % in July, the lowest since January 2022.

We got a bit more data from the UK last week. Tuesday's labour market data disappointed. The unemployment rate rose to 4.2 %.

The less important news from the US was Thursday's jobless claims, which came out surprisingly positive for the USD.

This week will be a bit weaker.

On Tuesday, we will focus on Japanese core inflation data, which will be released at 7:00.

Sources: