Hello everyone, we are sending you the last summary and outlook of this month. We wish you many successful trades for the new month!

At Thursday's meeting, the European Central Bank raised interest rates by 25 basis points, the ninth rate hike in a row.

The most anticipated event the market focused on was Wednesday's Fed monetary policy meeting

Full report here:

https://www.federalreserve.gov/newsevents/pressreleases/monetary20230726a.htm#

On Wednesday, we still focused our attention on Australian inflation data, which may provide a clue for this week's Tuesday session.

This week will again be richer in incoming data. Here is a summary of the most important ones:

Tuesday, August 1: AUD - Reserve Bank of Australia meeting (6:30)

EUR - labour market data (11:00)

Sources:

Welcome to the regular Monday recap of last week's fundamentals, in which inflation played a major role.

Let's take a look at the most important things together.

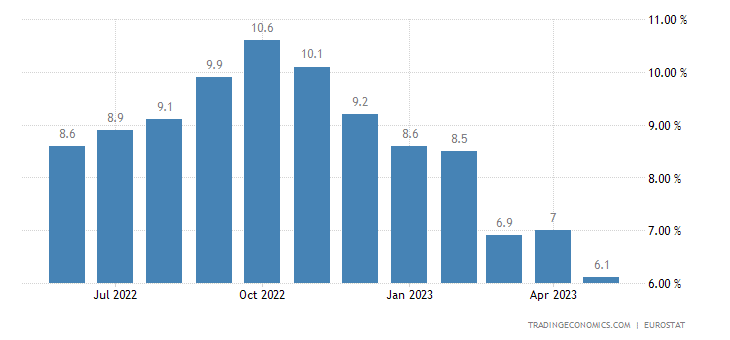

Wednesday's data on the current inflation rate confirmed the European Central Bank's hawkish stance.

On Wednesday, inflation data also came from the UK, which disappointed the market slightly.

Thursday's report on the number of Americans filing for unemployment benefits fell to 228,000 from the previous week.

The Australian labour market showed surprising numbers on Thursday, to which AUD strengthened in the first reaction.

The more interesting events in fundamental will be brought to us in the second half of the week, in which we will focus on these events:

Wednesday 26 July - Australian inflation rate (3:30)

Sources:

Welcome to our regular recap of the most important fundamentals we have been following over the past week.

The latter was marked by central banks, which this time did not surprise the markets so much.

This week, however, will be rich in fundamentals.

Read on to keep up to date

Tuesday's UK leveraged market data was rather negative, which is not a positive signal.

On Wednesday, we turned our attention to the Reserve Bank of New Zealand (RBNZ) meeting, which left the key interest rate unchanged for the first time in the rate hike cycle.

Wednesday's data on the US inflation rate showed us a decline that was still below market estimates.

Wednesday's Bank of Canada (BoC) meeting brought a 25 basis point hike, as expected.

TIP: Read the full Bank of Canada report

https://www.bankofcanada.ca/2023/07/mpr-2023-07-12/

This trading week will be rich in incoming inflation data, which we will certainly turn our attention to.

Tuesday, July 18 - Canadian inflation rate (14:30)

Sources:

Welcome to our regular Monday recap of the most important fundamentals we've been following over the past week.

Let's recall a few highlights together!

Thursday's retail sales data from the euro area brought no change.

We got more on the US dollar (USD) last week and the volatility in the market was noticeable. On Thursday, the market got excited on a positive surprise in the form of ADP.

Friday's labour market data, unlike the US dollar, was positive for the ,,Canadian,,.

The Reserve Bank of Australia (RBA) left its key interest rate unchanged at 4.1 % at its meeting on Tuesday.

This week we will be looking at the fundamentals which will mainly impact GBP, USD, NZD and CAD.

Tuesday, July 11 - UK labour market 8:00

Sources:

Welcome to our regular Monday recap of the highlights from the last trading week. This one was mostly about inflation and outputs from key central bank policymakers.

Let's recall the events together to keep us in the loop.

On Wednesday, we watched ECB President Christine Lagarde speak at the conference along with other central bankers.

Powell said the process to achieve % inflation still has a long way to go.

"The Canadian," was also in our sights because of the coming inflation numbers. It showed weaker numbers.

This week we will focus our attention mainly on the upcoming events concerning AUD, USD and CAD.

Sources:

Welcome to our regular Monday recap and outlook. Last week was a surprising one, both from central banks and in global events. So let's take a look together at what happened and what the current trading week will bring.

On Wednesday, the market was awaiting data on the current inflation rate in the United Kingdom. Consumer Price Index (CPI) growth held steady in May, but above market expectations, which were looking for a slight decline.

On Wednesday and Thursday, Fed President Jerome Powell testified before the Joint Economic Committee in Washington. The testimony consists of two parts: the first part is a prepared statement, after which the Committee will conduct a question and answer session. During the question-and-answer portion of the testimony, there may be strong market volatility.

At Thursday's meeting, the Swiss National Bank raised the key interest rate by 25 basis points.

The Czech National Bank left the interest rate unchanged, as expected.

In the weekly telegram group we sent our technical outlook on the USD/CZK currency pair, where we saw a potential zone to buy (long).

The current trading week will be a bit weaker. We will focus our attention on the following events:

Tuesday 27th - Canadian inflation rate (14:30)

Sources:

The regular Monday recap is here! Last trading week was busy with central banks and inflation. Let's recap the highlights together to keep us in the loop for the current week!

On Wednesday, we focused our attention on the monetary policy meeting of the European Central Bank (ECB), which raised the key interest rate by 25 basis points to 4 %.

The UK unemployment rate surprised market estimates and fell from 3.9 % to 3.8 %.

The attention of the entire market was focused on Wednesday's Fed meeting, which, as expected, left rates unchanged.

On Thursday morning we got data from the Australian labour market, which was on a positive note and surprised above market estimates.

In this trading week, we turn our attention to the events listed below:

Wednesday: 8:00 - UK inflation

16:00 - Fed Chair Powell addresses the committee

Sources:

Welcome to our regular Monday recap of the most important things that happened last week.

This trading week will also bring interesting events.

Read on to keep up to date!

Tuesday's meeting of the Reserve Bank of Australia brought surprises for the second consecutive day.

On Wednesday, we focused our attention on the Bank of Canada meeting, which unexpectedly raised the key interest rate by 25 basis points.

At the start of the week, we were expecting incoming Swiss inflation data, which was estimated to have come in lower.

This week will again be marked by inflation and central banks.

On Tuesday, we will focus our attention on the current inflation rate in the US, which will come at 2:30 p.m. and the markets will certainly be waiting for this data, as the Fed's monetary policy meeting is scheduled for a day later on Wednesday.

Sources:

Welcome to our regular Monday recap of the most important fundamentals.

Last week, we focused mainly on the incoming data from the euro area and the US, which were surprising.

Read on to keep up to date!

Last Thursday, we turned our attention to the preliminary inflation numbers from the euro area, which came in below.

The end of the week closed with the US labour market numbers, on which the US dollar strengthened.

This week we will focus mainly on central bank meetings.

The Reserve Bank of Australia meets on Tuesday at 6:30am, where the market expects a pause in rate hikes.

Sources:

Welcome to Monday's regular recap of the fundamentals that brought volatility in the past trading week.

The biggest surprises came from the Reserve Bank of New Zealand and the United Kingdom.

Read on to keep up to date!

According to the preliminary estimate, the HCOB Composite PMI fell to a three-month low in May 2023.

On Wednesday, we focused on the incoming inflation data from the UK, which was surprising.

Tuesday's US PMI data came in above market estimates.

The main event of last week was the meeting of the Reserve Bank of New Zealand, which brought volatility to the market with its rhetoric, and in response the New Zealand dollar began to weaken.

The start of the week is likely to be weak in the UK and the US through the holidays.